2021 has started off strong, unemployment continues to be reduced and a record high stock market. As the COVID-19 vaccinations are increasing, there seems to be an optimism as the year goes on.

Significant increase in industry confidence has occurred. Confidence has increased over 25% since last quarter.

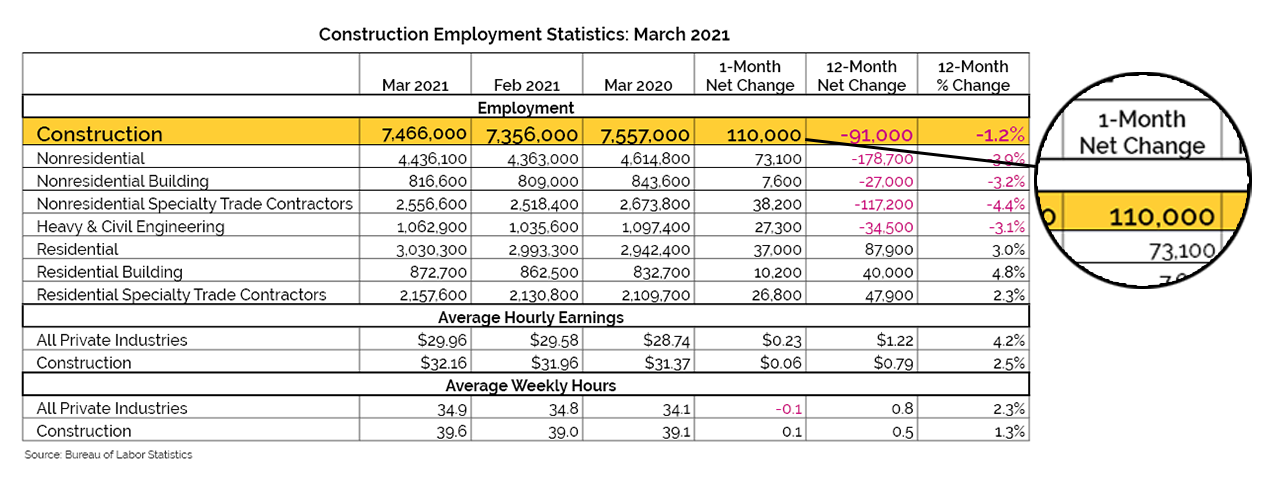

Construction jobs continue to recover. Closing the 12-month percentage change nearly in half.

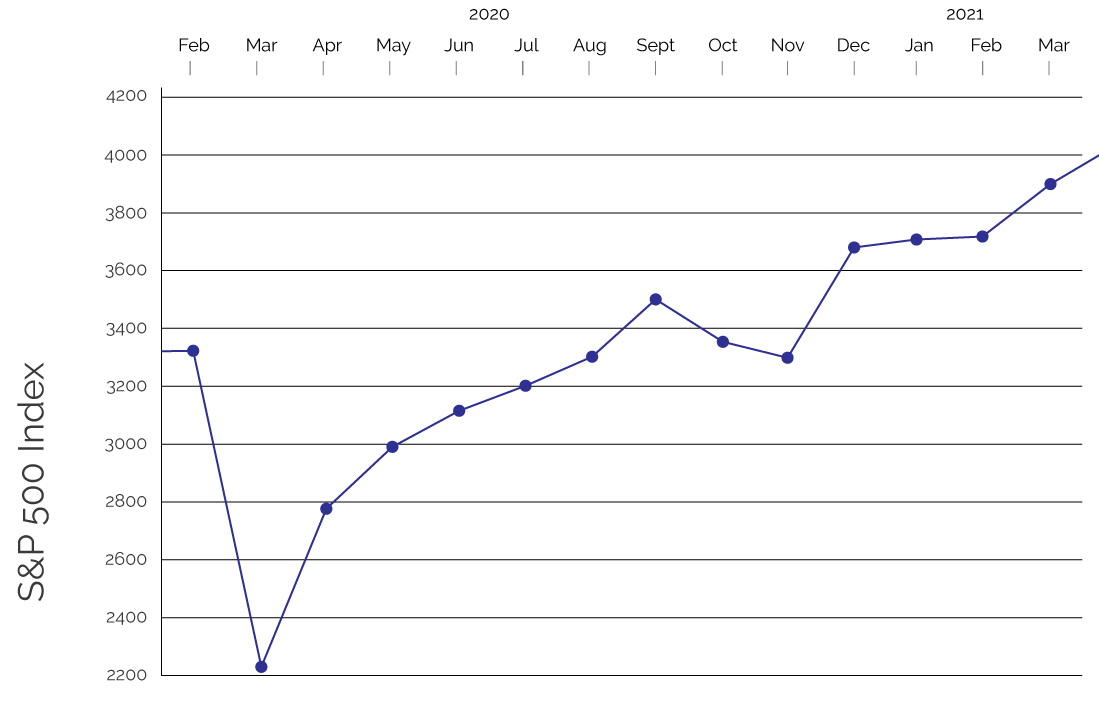

The stock market continues to make gains and historic milestones. Potentially due to confidence as vaccinations increase as well as government stimulus intervention.

Inflation for Q1 2021 is increasing from the previous year as the recovery continues. In addition, inflation in construction is higher than the national average due to construction material reduced production during the peak of COVID-19 while simultaneously demand increased as many homeowners started to improve their homes to better suite their remote working needs as well as increased home leisure activities.

Unemployment has continued its downward trajectory. Unfortunately, the employment recovery appears to be leveling off. Many jobs in the service industry have not and may not recover fully in the near future.

Due to material increases and difficulty procuring materials, it is advantageous for owners to start planning projects now. Hopefully, as the year closes out and projects move to the bidding phase, material issues will have stabilized as we move to a post COVID 19 normal.

![]()

![[AUTHOR]](https://www.slamcoll.com/images/people/Square__NBernier.jpg)